Uncategorized

SKILLS THAT WILL BE IN DEMAND IN NEXT 5 YEARS.

Why is learning skills that will be in demand in next 5 years is Important..?

With rapid advancements in technology, automation and artificial intelligence, the job market is changing faster than ever. Many traditional jobs are disappearing, while new opportunities are emerging that require completely different abilities. If you want to stay relevant, you must learn the skills that are in demand in next 5 years. In this article, you will discover the most important future skills you should start learning today to secure your career and income.

Why does learning Future Skills Matter..?:

The job market is evolving faster than ever. Automation, artificial intelligence and digital transformation are reshaping industries. According to industry trends, many current jobs may disappear. But new roles will emerge that require advanced and adaptable skills. So, the question is – Are you preparing for the future or falling behind?

Top Skills That Will Be In Demand In Next 5 Years:

Over the next five years, the most in – demand skills will blend advanced technology with human centric abilities, specifically, generative AI, data analysis, cybersecurity and cloud computing. To complement these, professionals must master adaptability, critical thinking and digital storytelling. Here are the top skills projected for the next 5 years.

TOP TECHNICAL SKILLS THAT WILL BE IN DEMAND IN NEXT 5 YEARS:

Artificial Intelligence (AI) and Machine Learning (ML) :

AI has moved beyond experimental projects. It is now integrated into everything from personalised health care diagnostic to marketing to fraud detection in the banking system i.e. completely transforming everything. Companies are actively hiring people who understand AI tools and systems.

Why Skills are in Demand in Next 5 Years Matters:

➔ Workers with AI skills and expertise have salary hikes of over 54%, enjoying the highest pay. It has high paying opportunities.

➔ Companies across industries and all sectors are desperate for hiring AI talent.

➔ The AI market continues its explosive growth trajectory as it is a future- proof skill.

How to Learn Skills That will be in Demand in Next 5 Years:

❖ Learn basics of AI and ML.

❖ Take beginner friendly online courses.

❖ Explore tools like Chat GPT, automation platforms.

❖ Google cloud professional machine learning engineer.

❖ Microsoft Azure AI engineer associate.

Data analysis and data science:

Data is the new oil. Companies rely on data to make smarter decisions. Every business generates huge data but only few can actually make use of it. This is the place where data scientists enter. From e-commerce platforms optimising prices to agricultural companies prediction crop yields, data-driven decisions are making or breaking the business.

Why Skills Are in Demand in Next 5 Years Matter:

➔ There is a very high demand for data scientists in India as well as in the global market from health care to entertainment.

➔ India’s data analytics industry continues rapid expansion.

➔ Data scientists are valuable in every industry and they are paid with excellent salary packages.

How to Learn Skills That will be in Demand in Next 5 Years:

❖ Excel / Google sheets.

❖ Structured Query Language ( SQL).

❖ Data visualization.

❖ Applied data science with Python.

❖ Google data Analytics professional certificate.

Cyber security and Ethical Hacking:

Cyber security is the broad practice of protecting systems, networks and data from digital attacks and Ethical Hacking is a specialised, proactive subfield within it. As the digital footprints expand, Cyber threats multiply. The need to protect sensitive data and crucial infrastructure has made cybersecurity one of the most important and recession – proof fields.

Why Skills Are in Demand in Next 5 Years Matter:

➔ Cyber threats don’t stop during economic crises.

➔ The talent shortage is severe and the situation is getting worse.

How to Learn Skills That will be in Demand in Next 5 Years:

❖ Certified Ethical Hacker from EC- Council, penetrates testers, security analyst.

❖ Comp ITA security+

❖ Understanding of operating systems ( Linux / Windows); programming languages and security protocols.

❖ Demand in sectors like finance, defence and Tech.

❖ CISSP – Certified Information System Security Professional.

UI / UX Design:

A UI / UX designer creates functional appealing digital interfaces by combining user research ( UX) with visual design (UI). The focus is on user needs, wire framing, prototyping and testing to ensure intuitive experiences. Good design = better use experience; that is why UX / UI designers are valued.

Why Skills Are in Demand in Next 5 Years Matter:

➔ It is a creative + technical field.

➔ UX designers are creators with skills.

➔ UI designers are technical with skills.

➔ High demands in start-ups and tech companies.

How to Learn Skills That will be in Demand in Next 5 Years:

❖ User psychology

❖ Design tools ( Figma, Adobe XD)

❖ Wire framing.

Digital marketing:

Digital marketing is the promotion of brands, products or services using online platforms, electronic devices and internet-based technologies. It enables data-driven, cost effective outreach compared to traditional marketing. Companies are fighting fierce battles for online visibility, making skills in SEO, social media marketing and data-driven campaigns essential.

Why Skills Are in Demand in Next 5 Years Matter:

➔ Every business needs customers and today everyone is online.

➔ Digital marketers can work from anywhere, and so are in constant demand.

➔ Great for starting your own business.

➔ High freelance opportunities.

How to Learn Skills That will be in Demand in Next 5 Years:

❖ Search Engine Optimization (SEO).

❖ Content marketing.

❖ E-mail marketing and marketing automation.

❖ Pay-per-click (PPC), advertising on Google and other social media platforms.

❖ Social media marketing and growth.

❖ Google Ads certification.

❖ SEMrush academy certificate.

❖ Meta blueprint certification.

COGNITIVE AND SOFT SKILLS:

Critical Thinking and Problem Solving:

Not all skills are technical. Companies even need people who can think, adapt and solve problems. Critical Thinking is the objective analysis and evaluation of information to form a reasoned judgement, while Problem Solving is the process of implementing solutions to overcome obstacles. Together they get involved in defining issues, analysing data,identifying the biases and acting decisively to achieve goals.

Why Skills Are in Demand in Next 5 Years Matter:

➔ Essential for navigating complex situations such as Managing.

➔ Without Critical Thinking, solutions may be ineffective.

➔ Without Problem Solving, analysis remains purely theoretical.

➔ To understand the root cause of a problem.

➔ Together or separately it helps in any career.

➔ Makes you stand differently.

➔ It is hard to replace with AI.

How to Learn Skills That will be in Demand in Next 5 Years:

❖ Coursera Critical Thinking course.

❖ Solving Problems with Creative and Critical Thinking – IBM

❖ University backed certificate.

Emotional Intelligence (EQ) and Human Centric Abilities:

Despite the rise of automation, Human Centric Abilities are irreplaceable. Emotional intelligence includes Self – Awareness, Empathy and strong Communication will set professional apartment. As remote work and cross – cultural teams become more prevalent, these interpersonal abilities like leadership, communication, adaptability, and collaboration are increasingly more valuable and drive long – term career growth.

Why Skills Are in Demand in Next 5 Years Matter:

As AI handles technical tasks, the skills that can’t be automated, like –

➔ Understanding your own emotions.

➔ Managing stress and reactions.

➔ Empathize with others.

➔ Communicate effectively.

➔ Building relationships.

➔ Leading teams.

➔ Creative problem solving.

How to Learn Skills That will be in Demand in Next 5 Years:

❖ Effective communication – Join toastmasters club for public speaking and communication.

❖ Practice active listening in every interaction.

❖ Take leadership and management courses on LinkedIn learning.

❖ Volunteer for cross – functional projects.

BONUS FAST GROWING SKILLS THAT WILL BE IN DEMAND IN NEXT 5 YEARS:

Entrepreneurship and Business Skills:

More people are choosing this skill to start their own businesses or side hustles. This skill matters as it provides financial freedom, creative freedom and unlimited earning potential.

Cloud computing:

The migration to cloud infrastructure is not coming, it has already happened. It is a demand delivery of IT resources such as servers, storage, data base and software – over the internet with pay – as – you – go pricing. Instead of buying and maintaining physical data centres, users access technology services on an as needed basis from providers like AWS, Google cloud, Microsoft Azure. Businesses now rely on cloud computing for security, scalability and cost efficiency.

Blockchain technology:

Blockchain is revolutionising way more than just Cryptocurrency. It is a decentralised database or ledger that securely stores records across a network of computers in a way that is transparent, immutable and resistant to tampering. It “block” contains data and the blocks are linked in a chronological chain and hence creating entirely new paradigms for trust in digital transactions.

Renewable energy and green technology:

India marches towards its ambitious climate goals. Renewable energy and green technology focus on using naturally replenished – solar, wind, hydro, geo thermal- to generate sustainable heat and electricity while minimizing environmental impact. Driven by decarbonisation goals, technologies like Solar PV and wind are expanding rapidly, reducing reliance on fossil fuels and driving significant economic growth and job creation.

Your 6 month plan to learn skills that will be in demand in next 5 years:

➔ Pick one skill based on your interest.

➔ Use free platforms ( blogs , courses,YouTube).

➔ Practice consistently.

➔ Build small projects .

➔ Stay updated with trends.

➔ Network actively in your target industry.

➔ Share your work and start applying.

REFERENCE:

https://share.google/bfzmbS5XD604XEluJ

REFERENCES:

https://sumermannwings.com/emotional-intelligence-superpower-guide/

https://sumermannwings.com/emotional-spending/

Conclusion:

The future is not something you wait for – it’s something you prepare for. The skills that will be in demand in next 5 years are not just about technology – they are a combination of technical expertise and human abilities like emotional intelligence, critical thinking and communication.

Don’t wait for the perfect time. Start today, build consistently and become the person the future needs because – the future doesn’t belong to the smartest person – it belongs to those who are willing to learn, adapt and take action.

<!– wp:post-terms {“term”:”post_tag”,”prefix”:”skills that will be in demand in next 5 years\u003cbr\u003efuture skills\u003cbr\u003eartificial intelligence\u003cbr\u003edata science\u003cbr\u003ecybersecurity\u003cbr\u003edigital marketing\u003cbr\u003ecareer growth\u003cbr\u003ecritical thinking\u003cbr\u003eemotional intelligence\u003cbr\u003eethical hacking\u003cbr\u003ecloud computing\u003cbr\u003efuture jobs 2026\u003cbr\u003eblockchain technology\u003cbr\u003efuture skills\u003cbr\u003ein-demand skills\u003cbr\u003eskills for future jobs\u003cbr\u003ehigh income skills”} /–>

![]()

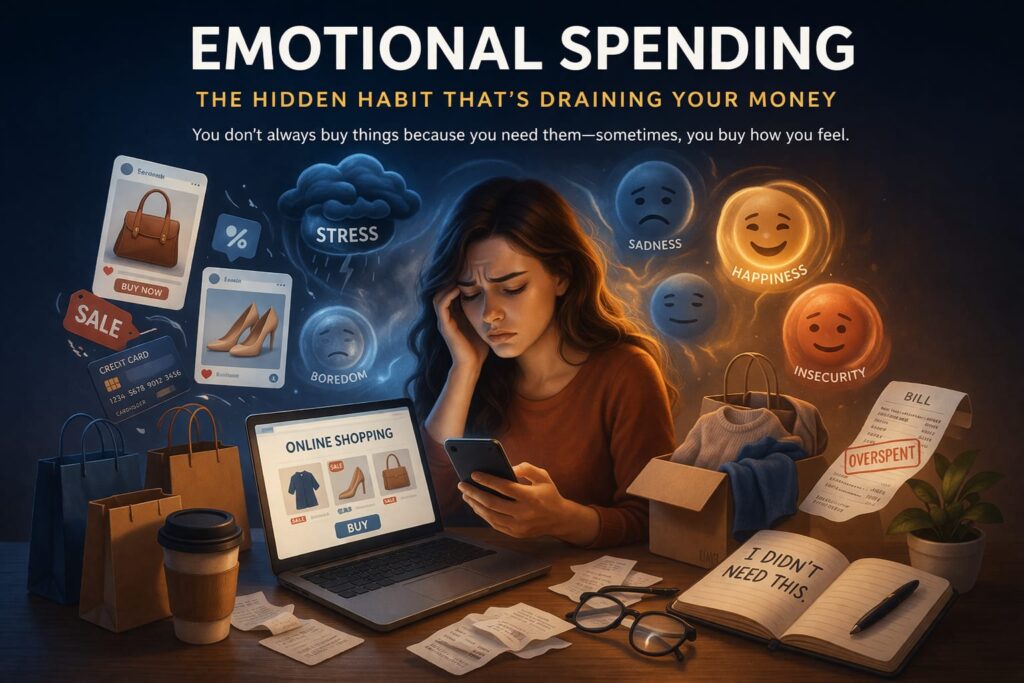

Money decisions are rarely just about numbers – the reality is all about feelings. Stress, happiness, insecurity and even boredom influences the habit of money you spend. Emotional spending is not just a bad habit, it is a psychological pattern that can quietly keep you stuck in the cycle of financial struggles.

In my previous blog, we explored the difference between the Rich Mindset and the Poor Mindset. But mindset alone isn’t enough – your daily spending habits reveal the truth. And emotional spending is one habit that can quietly hold you back from building real wealth. It is one of the most common yet overlooked reasons why people struggle with money.

What is Emotional Spending:

Emotional Spending is the act of spending money based on feelings rather than the actual needs. Instead of making logical financial decisions, triggered emotions like stress, sadness, boredom or excitement takes control. Emotional Spending, often called “retail therapy”, is an impulsive coping mechanism used to gain temporary pleasure, through dopamine release, but often leads to regret, financial strain and debt.

“It’s not about what you buy – it’s about why you buy it.”

For examples:

★ Shopping after a stressful day.

★ Ordering expensive food to feel better.

★ Buying things to impress others.S

★ Treating yourself frequently.

Common Triggers Of Emotional Spending:

Understanding your triggers is the first step to controlling the spending habit.

Retail Therapy: Shopping online or in-store after a stressful day to feel better.

Stress and Anxiety: Purchasing unnecessary items like clothes or gadgets, after a difficult work day to feel in control or comforted.

Boredom Buying: When you have nothing to do, spending becomes entertainment. Making online purchases while browsing, simply because of a lack of stimulation.

Fear Of Missing Out (FOMO) : Buying items due to urgency created by sales, limited timeoffers or social pressure.

Social Media Influence: Seeing other’s lifestyles can create pressure to spend and “keep up”.

Celebration Splurging: Spending beyond one’s budget because of a high-energy positive emotions, such as raise or personal success.

Rewards and Celebrations: “I deserve this”- this can become a dangerous habit of overuse.

Synonyms and Related terms of Emotional Spending:

Impulsive buying/ Spending: Making unplanned, in-the-moment purchases.

Retail Therapy: Using shopping to improve one’s mood.

Comfort Spending: Spending to soothe oneself.

Doom Spending: Spending to cope with anxiety about the future or economic conditions.

Compulsive Shopping (chronic/ severe): Compulsive buying is a mental health condition characterized by uncontrollable, excessive urge to shop, resulting in emotional distress and financial problems.

The Hidden Consequences of Emotional Spending:

Emotional spending may feel harmless, but overtime it creates serious financial problems.

The Debt Stress Cycle: Initial gratification turns into long- term financial stress, which often triggers even more emotional spending, worsening debt and reducing financial discipline like- use of credit cards, “buy-now-pay-later”.

Psychological Toll: Beyond debt, this habit causes deep regret, anxiety, “buyer’s remorse “and low self-worth.

The “Secret” Spending: People often hide purchases from partners – creating tension in relationships.

Chronic Financial Stress: Emotional Spending often leads to neglecting saving for emergencies, building retirement funds and ruining long -term financial goals, resulting in fragile financial situations.

Living Paycheck to Paycheck: Regardless of income level, emotional spending often results in spending all available funds.

This Cycle Repeats Itself:Emotion ~ Spending ~ Regret ~ Stress ~ More Spending.

Emotional Spending and Mindset:

Emotional Spending is the act of making purchases driven by feelings rather than needs. It acts as temporary ‘retail therapy’ giving us a false sense of control. Breaking this cycle requires identifying emotional triggers, practicing mindful budgeting and delaying purchase habits.

Key aspects of Emotional Spending and Mindset:

➢ Uncontrollable buying habits: Extreme cases, also known as compulsive buying disorder, involve persistent that causes significant life disruptions.

➢ Stress and Anxiety: Shopping offers a sense of control where life feels chaotic.

➢ Sadness: Scrolling through apps provides instant stimulation and novelty.

➢ Positive emotions: Spending to celebrate or reward oneself (“I deserve this”).

➢ Mindset: A rich mindset focuses on discipline, long term thinking goals and control over finances. A poor mindset focuses on instant gratification and emotional decisions. Emotional spending is often a sign of poor financial mindset.

How to stop Emotions spending (practical tips):

Transforming your relationship with money requires moving from reactive impulses to intentional choices. Controlling the emotional spending is a step towards developing a Rich Mindset. The following are the key strategies to break the cycle of emotional spending:

❖ Follow the 24-hour rule: Wait at least 24 hours before purchasing any non-essential or unplanned item. This ‘cooling off’ period allows the initial emotional wave to pass.

❖ Track your spending: Awareness helps you understand where your money is going (i.e) before any purchase, ask yourself “ Am I buying this because I need it” or ” because of how I feel right now”.

❖ Identify triggers: Recognise if you spend when you are stressed, sad, lonely or bored and address the underlying emotion directly.

❖ Add friction to purchases:

➔ Delete saved credit card info from browsers.

➔ Unsubscribe from promotional e-mails and delete shopping apps.

➔ Use cash for discretionary spending to make up for the loss of money.

❖ Replace the habit: Replace the emotional spending on shopping high with free alternatives like a 15- minute walk, calling a friend, journalising your thoughts, quick meditation or reading books.

❖ Create a ‘ Fun budget’: Allocate a specific small amount of “fun money” in your budget for guilt – free treats. This allows for small rewards without derailing your main financial goals.

REFERENCE :

https://share.google/KvgDU7jtxr6CwzDRX

REFERENCES TO EMOTIONAL SPENDING

https://sumermannwings.com/rich-mindset-vs-poor-mindset/

https://sumermannwings.com/emotional-intelligence-superpower-guide/

https://sumermannwings.com/psychology-of-money-2/

Real Life Examples of Emotional Spending:

1. Imagine you have a stressful day at work. Instead of ordering expensive food or shopping online, you can take a walk, relax or cook a simple meal.

Same Emotion, different response – better financial outcome.

2. Overspending during Celebrations. Birthdays, festivals or small achievements turn into an excuse to spend more than planned.

3. Buying Things After Seeing Social Media. You see your favourite influencers or any of your friends posting new outfits, phones or even any trip- you feel the urge to spend time “keeping up”.

4. “ I Deserve This” purchases. After working hard, you reward yourself frequently -even if it affects the budget.

5. Spending To Impress others – Buying branded clothes, expensive gadgets or treating your friends just to maintain your status.

6. Using Credit cards without Thinking. Swiping a card feels easy at the moment, but later leads to stress when the bill arrives.

7. Panic buying during Fear Or Uncertainty. Buying unnecessary items in bulk during sales or uncertain situations.

8. Buying Discounts You Don’t Need. Purchasing items just because they are “on sale”, even if they are not useful.

If you relate to even a few of these, chances are Emotional Spending is affecting your financial life more than you think.

Conclusion: Control Your Emotions, Control Your Money:

Emotions are a natural part of life – but they should not control your financial decisions. Emotional Spending may give short-term happiness, but it often leads to long – term stress. The key is not to eliminate emotions, but to be aware of them and respond wisely.

Remember: Financial success is not about how much you earn – it’s about how wellyou control your habits.

Start small, stay consistent and take control of your spending – because when you control your emotions, you take care of your financial future.

![]()

Rich Mindset vs Poor Mindset.. Means what..?

Have you ever wondered why some people build wealth, while others struggle financially, even when they earn the same income? The difference has little to do with luck, intelligence or education. In fact, it comes down to the powerful factor mindset. The way people think about money shapes their financial decisions everyday. The strategy lies within the rich mindset and the poor mindset.

Those with a rich mindset tend to focus on opportunities, growth and long-term wealth. In contrast, a poor mindset often focuses on limitations, short-term pleasure and fear of financial risk. Understanding the difference between these two mindsets, can completely change the way to manage money and build wealth. “In this article, we will explore rich mindset vs poor mindset and how it impacts your financial future.

“What is a Rich Mindset in Rich Mindset vs Poor Mindset?”

A rich mindset is a proactive, growth -oriented perspective, a long term approach to life and finances that view money as a tool for investment, appreciates abundance, growth and opportunity, embraces instant gratification and calculated risks over scarcity and fear.

“Here are key habits in rich mindset”:

● Abundance mentality: Believes there are always opportunities, rather than thinking wealth is limited.

● Accountability: Taking full responsibility for actions and financial situations, rather than blaming others. ( Victim mentality).

● Life long learning: Actively seeking to learn new skills to improve and grow.

● Long term thinking: Trading immediate pleasure (instant gratification) for future benefits, such as investing instead of over spending.

● Creating value: Focusing on producing or creating value, products or services that help others.

● Calculated risk & resilience: Viewing a failure as a learning opportunity rather than a reason to quit.

Related terms to Rich Mindset:

● Abundance mentality

● Growth mindset

● Entrepreneur mindset

● Success mindset

● Wealth consciousness

● Financial Intelligence

● Proactive attitude

Examples of Rich Mindset:

● Instead of asking, “How can I afford this?” You ask “How can I produce enough value to earn this?”

● Instead of avoiding projects due to fear, take a ‘calculated risk’ to invest in a business opportunity.

Understanding the Rich Mindset and their long term thinking in Rich Mindset vs Poor Mindset:

People’s thoughts about money are highly subjective and often assumed by their financial situation, opportunity, luck or any external factors – but the truth lies in how the wealthy think. Their habits, mindset and principles create a framework that not only helps them accumulate their wealth but also sustain it over time. In this article, we will understand the psychological traits, habits and mental strategies that define a wealthy individual and their long term thinking which contributes to their financial success.

Rich Mindset/Growth Mindset:

The psychologist Carol Dweck explained that the psychology of wealth is about growth mindset. Wealthy individuals accept the challenges and see failure as an opportunity for learning. Viewing obstacles as unconquerable, they see them as stepping stones to success.

Long term thinking of Rich Mindset:

● Seek opportunities for self – improvement and continuous learning.

● Seeking challenges as opportunities for growth.

Parsimony and mindful spending:

Many rich individuals live below their means and focus on value over luxury. They might spend on high valued products, but as they are mindful, they know where their money goes. This Parsimony allows them to accumulate and reinvest their wealth.

Long term thinking of Rich Mindset:

● Track their spending and ensure their lifestyle within their means.

● Focus on long term wealth accumulation.

Network and relationship:

An individual’s effort cannot build wealth – it depends on an individual’s network and relationships. A wealthy individual is always surrounded by business partners, mentors, advisors who help in growing their wealth.

Long term thinking of Rich Mindset:

● Build and maintain a strong professional network.

● Seek out mentors who can offer guidance and insights.

Financial literacy and education:

The wealthy individuals will prioritize financial education.They will understand the concept of how money works. From the basics of budgeting tocomplex things like tax, investing, retirement planning, optimization, market trends and opportunities, wealthy individuals will seek to educate themselves by gaining knowledge and staying updated as per the current scenario.

Long term thinking of Rich Mindset:

● Invest in education as a means of long term wealth accumulation like reading books and attending seminars.

● Regularly update their financial strategies based on new information.

“What is a Poor Mindset in Rich Mindset vs Poor Mindset?”

A poor mindset also known as scarcity mindset is a psychological framework rooted in scarcity, believing that resources, opportunities and success are limited. It is an unconscious, fear based approach to life focused on limitation, immediate gratification and avoiding risk rather than growth.

Here are Key habits of a Poor Mindset:

● Fear based decision: Avoiding investments in education, networking or business opportunities due to fear of failure.

● Victim mentality and complaining: Frequently blaming others or the circumstances for financial failing, rather than taking responsibility.

● Instant gratification: Prioritizing immediate consumption and comfort over saving, investing or any other long term planning.

● Scarcity thinking: Believing resources (time, money, opportunity) are limited and someone else’s gain in their loss.

● Underinvestment in self: Focusing on saving money rather than investing in personal growth, skills or knowledge.

Related terms of Poor Mindset:

● Scarcity mentality

● Poverty consciousness

● Fixed mindset ( regarding finances)

● Short termism

● Victim mentality

Common examples:

● Believing money is meant to be spent, not invested.

● Feeling trapped in a financial situation.

● Comparing self with others and feeling perpetually behind.

Common limiting Beliefs about Money in Rich Mindset vs Poor Mindset:

A poor mindset is characterized by scarcity thinking, fear based financial decisions and short-term focus, which can trap individuals in a cycle of financial struggles regardless of their actual income.

● Money is the root of all evils: Viewing wealth as immoral creates subconsciousself- sabotage.

● It takes money to make money: A belief that keeps people from starting business or investing small amounts, waiting for a large capital that never comes.

● Money is scarce / hard to make: A scarcity mindset leads to hoarding resources or avoiding risks, rather than generating more value.

● My family has never been rich: A belief that poverty is a hereditary fate rather than the condition that can be changed.

Short -term thinking traps of Poor Mindset:

The poverty mindset focuses on immediate gratification rather than long-term security.

❖ Impulsive Spending: Spending money, for the sake of maintaining status, immediately on luxury or entertainment instead of saving or investing for the future.

❖ Lottery Mentality: Looking for “get – rich – quick” schemes or waiting for a windfall rather building sustainable wealth through strategy and patience.

❖ Ignoring Financial Planning: Believing that the budget is only for rich people. Tracking expenses due to fear or overwhelming feelings about a lack of money.

Financial Struggles of a Poor Mindset:

These habits are often lead to repeated financial crises, regardless of income changes :

★ The Debt trap: Using credit cards for non- essentials to cover monthly expenses, leading to high interest debt that reduces future freedom.

★ Living Paycheck to Paycheck: Regardless of income level, a scarcity mindset often results in spending all available funds.

★ Fear Based Investing: Being too conservative with money due to fear loss, which results in losing purchasing power to inflation.

“Key Differences in Rich Mindset vs Poor Mindset Explained”:

A rich mindset focuses on growth and building assets, whereas the poor mindset focuses on scarcity and limitations.

Key difference between the Mindset:

● View of money:

Rich Mindset: View money as a tool to create wealth through investments and savings.

Poor Mindset: View money as a source of income to be spent on liabilities and immediate consumption.

● Time Horizon:

Rich Mindset: Focuses on long term goals, sacrificing short term goals for future success.

Poor Mindset: Focuses on short term growth, prioritizes instant gratification and immediate comforts.

● Learning and Growth:

Rich Mindset: Possess a “growth mindset”, constantly learning and developing new skills.

Poor Mindset: Often believes as it “knows enough” and is closed-minded.

● Perspective on Risk and Failure:

Rich Mindset: Rich embraces calculated risk and sees failure as a learning opportunity.

Poor Mindset: Fears change and risks, avoiding potential failure, often resulting in stagnation.

● Action and Accountability:

Rich Mindset: Rich mindset is proactive, takes initiative and responsibility for their financial strategies.

Poor Mindset: Often adopts a “victim mentality”, complains about unfairness and blaming external factors for their financial situations.

REFERENCE:

https://share.google/qyLVA9WsNnapFTKyi

Reference for Rich Mindset vs Poor Mindset:

https://sumermannwings.com/emotional-intelligence-superpower-guide/

https://sumermannwings.com/psychology-of-money-2/

“Below is a clear comparison of rich mindset vs poor mindset:”

| Aspect | Rich Mindset | Poor Mindset |

| Thinking Style | Focuses on growth and opportunities | Focuses on problems and limitations |

| Money Belief | Money is a tool to build wealth | Money is scarce and hard to earn |

| Spending Habit | Invests in assets and education | Spends on liabilities and pleasure |

| Time Perspective | Long -term thinking | Short-term thinking |

| Risk Approach | Takes calculated risks | Avoid risks due to fear |

| Learning | Continuously learns and improve | Avoid learning new financial skills |

| Income Strategy | Multiple income sources | Depend on one source of income |

| Reaction to failure | Learns from mistakes | Blames others |

| Attitude towards others success | Gets inspired | Feels jealous or discouraged |

CONCLUSION:“Understanding rich mindset vs poor mindset can completely change your financial future.”

In the end, the difference between the Rich Mindset and Poor Mindset is not about how much a person earns, but it shows the capability of a person, how the money and the opportunities are managed. The rich mindset will focus on long term growth, building assets and education, on the other hand, the mindset of the poor will always focus on fear, financial risks, short term satisfaction, limitations etc.

But the good news is mindset is something that can be changed. Developing better financial habits, learning skills, and thinking of money for a long term can definitely build healthier relationships with wealth. Remember one thing, financial success is not determined by income but it is defined by your decisions and attitudes we develop over the time.

<!– wp:post-terms {“term”:”post_tag”,”suffix”:”difference between rich and poor mindset\u003cbr\u003ehow mindset affects financial success\u003cbr\u003ehabits of rich vs poor people\u003cbr\u003ehow to develop a rich mindset\u003cbr\u003epoor mindset financial struggles\u003cbr\u003epsychology of wealthpersonal finance tips\u003cbr\u003ewealth building strategies\u003cbr\u003eself improvement\u003cbr\u003esuccess mindset\u003cbr\u003efinancial freedom\u003cbr\u003emoney habits\u003cbr\u003einvesting mindset\u003cbr\u003emillionaire mindsetgrowth mindset and wealth\u003cbr\u003eabundance vs scarcity mindset\u003cbr\u003efinancial success habits\u003cbr\u003emindset and money\u003cbr\u003ehow to build wealth mindset\u003cbr\u003efinancial education\u003cbr\u003elong term vs short term thinking\u003cbr\u003emindset for success\u003cbr\u003erich mindset vs poor mindset\u003cbr\u003erich vs poor thinking\u003cbr\u003ewealth mindset\u003cbr\u003epoor mindset\u003cbr\u003emoney mindset

![]()

YOUR FINANCIAL FUTURE

UNDERSTANDING THE PSYCHOLOGY OF MONEY:

Some people earn a high salary but still struggle financially, while few earn an average income but quietly build the wealth…How? Why do many intelligent people make poor financial decisions? How we can find the answer for this. The answer doesn’t lie in the financial knowledge but in something more deeper- that is in the psychology of money.

I have seen people who earn ten lakhs a month, but are not able to save a single rupee, while on the other side a person earning one lakh per month slowly builds wealth. What created the differences? The answer lies in the psychology of money.

Making money is not about just numbers, income or investment. It is mostly about how to use the money. The behaviour of utilising the money, makes one wealthy, while other remains broke. The difference, in behaviour of utilising the money, is not intelligence – it is the psychology behind how a person thinks about money.

WHAT IS PSYCHOLOGY OF MONEY?

THE MEANING OF PSYCHOLOGY OF MONEY:

The PSYCHOLOGY of money by Morgan Housel explores the emotions, behaviour and psychological factors that influence our financial decisions rather than intelligence or formulas or data-driven financial decisions. It also teaches that doing well with money is a soft skill where mindset, patience, having a long term perspective (like compounding), avoiding panic matters more than intelligence.

Key lessons and takeaways on how to make better financial decisions:

❖ Behaviour Over Intelligence: Financial success is not about what you know, it is all about how you behave.

❖ No One’s Crazy: People make financial decisions based on their experiences or reasons, but that seems rational to others.

❖ Wealth is what you don’t see: True wealth is not buying luxury (cars, gadgets), but it is the financial assets that have not been converted into things.

❖ The Power Of Compounding: Extraordinary results comes from small, consistent investment over long periods.

❖ Control Your Time: The highest dividend money pays is the ability to control your time and do what you want. Independence is the best financial goal.

❖ Room for an Error: The most important part of a plan is having a plan for when the plan is not going according to the plan.

❖ Save money: Building wealth has little to do with income or investment refunds, and a lot to do with your savings rate.

❖ Enough is Essential: The most difficult financial skill is getting the goal post to stop moving. Understanding when you have ‘enough’ prevents dangerous and excessive risk-taking.

❖ Play Your Game: Understand your own game, create your own strategy. Beware taking financial ideas from other people as they are playing a different game than yours.

❖ The Man in the Car Paradox: Spending money to show people what you have is the fastest way to have less money. No one is impressed with your possession as you are. Using wealth to signal status is the gap between your ego and your income.

WHY MONEY DECISIONS ARE EMOTIONAL..?:

Money decisions are deeply emotional because it directly impacts on survival, security, responses like fear, greed, desire etc.. Research suggests that up to 90% of financial choices are driven by emotions rather than logic. This happens because money is tied with maintaining social status and personal values, leading to behaviours like loss of aversion, over speeding for gratification.

Key areas which indicates why money decisions are emotional:

LOSS AVERSION: This is the psychological pain in which people often make impulsive decisions like the pain of losing money is far more intense than the pleasure of gaining, leading people to make poor choices.

DOPAMINE AND IMPULSE: Dopamine is a crucial brain chemical (neurotransmitter) that acts as a pleasure and reward, teaching you to repeat enjoyable behaviour, playing key roles in mood and movement. The dark side of dopamine is when you crave more for dopamine, you might start engaging in more pleasurable activities like addiction. Spending can trigger a“dopamine effect”, providing temporary emotional comfort.

FOMO MENTALITY: Following trends out of fear of missing out.

TRAUMA: Previous financial mistakes or successes influencing current decisions.

THE CONNECTION BETWEEN BEHAVIOURAL FINANCE AND WEALTH:

Behavioural finance explains how psychological cognitive biases like loss aversion, overconfidence and herd mentality – drive irrational financial decisions. But by recognising them, individuals and wealth creators can implement disciplined strategies to mitigate risks, improve investment and align financial choices with long term goals.

Key connections between Behavioural finance and wealth:

➢ Wealth management strategy: Using behavioural insights, to build portfolios, it helps the investors to stay focused during market volatility.

➢ Role of Advice: Working with a fiduciary advisor can help counteract the cognitive biases, acting as a “behavioural coach” to keep investors focused on long term goals.

➢ Generational wealth: Understanding behavioural biases allows for better, more structured and sustainable wealth transfer to future generations.

YOUR BACKGROUND SHAPES YOUR MONEY HABITS:

Our relationship with money is not created overnight. Your background shapes your money mindset by our childhood experiences, beliefs about security, scarcity or abundance, family beliefs, parental attitudes or financial struggles. Experiences such as witnessing financial instability or expressing“money doesn’t grow on trees” upbringing, dictate how you spend, save and perceive risk as an adult.

Important ways your background shapes your money mindset:

❖ Inherited money scripts: Rules thought from childhood – “debt is bad” or “investing is risky” – often influence your financial decisions.

❖ Family beliefs about wealth: Few families believe saving is the most important financial habit, while few families focus on enjoying money in the present. It is their beliefs which will influence the people to manage their finances later in life.

❖ Learning to build better money habits: By understanding how we are handling our money (i.e) money behaviours, we can develop habits like investing, saving and try to make money through our financial decisions.

❖ Social and Cultural Influence: For some cultures in our society, financial success is strongly associated with status and luxury, while for others it is associated with stability and security.

The Difference Between Being Rich And Being Wealthy:

Being rich is defined by high income and high spending on material possession (liabilities), resulting in a flashy lifestyle, while being wealthy is defined by high net worth, accumulation through investments, assets and unspent income. Rich is what you spend and Wealthy is what you keep.

Key Distinctions:

❖ Income vs Assets: Rich often require continuous high incomes so that they can spend for their flashy lifestyle, while wealth generates passive income as they use income to acquire assets that they appreciate.

❖ Visibility: Richness is often visible (what you spend), wealth is invisible (what you accumulate).

❖ Time vs. Money: Being rich means having a lot of money, but being wealthy means having time and freedom to work.

❖ Mindset: Rich is often about showing off, while wealth is about security, longevity and freedom.

❖ Measurement: Rich is measured by salary, wealth is measured by net worth (assets minus liabilities).

KEY LESSONS FROM THE PSYCHOLOGY OF MONEY:

The psychology of money by Morgan Housel teaches that financial success is more about behaviour than intelligence, emphasizing that wealth is often unseen. Controlling your time is the highest dividend and Compounding requires extreme patience.

REFERENCE: https://share.google/yBK25mVoouBMMeN5I

REFERENCE TO PSYCHOLOGY OF MONEY :

https://sumermannwings.com/emotional-intelligence-superpower-guide/

https://sumermannwings.com/how-to-invest-in-gold-in-india-2026/

Key Practical Lessons from the psychology of money:

★ Savings = Freedom and Control: Control on your emotional spending brings freedom which is the highest dividend for long- term happiness.

★ The Power of Time and Compounding: The most crucial element in investing is time. Compounding requires long term, consistent investment which will help increating intuitive wealth growth.

★ Developing money Mindset: Good investing does not require high intelligence, it requires a proper mindset with patience and staying invested over long periods.

CONCLUSION :

MASTER YOUR MIND TO MASTER YOUR MONEY:

At its core, financial success is not only about how much you earn, but it is about how much you think and behave with money. Your habits, emotions and experiences strongly influence saving, spending and investing the money. Many focus on strategies and numbers but overlook the psychological side of financial decisions.

The complete “PSYCHOLOGY OF MONEY”concept explains that the key to financial success is not about being the smartest person in the room, but about having the right mindset, behaviour and habit towards the money which can develop a healthy relationship with money and you can gain the power of building huge wealth.

In the end, mastering money begins with mastering your mind.

Mindset Improves = Financial decisions improves = True secret to long term Financial success.

![]()

CHAMELEONS

Chameleons are known for their rapid changing of colors. People believe that they change colors and camouflage against a background. But the truth is that they change color to regulate their temperatures or to communicate with other chameleons.

As chameleons cannot generate their own body heat, they change colors and adapt themselves to a favourable body temperature. For example, a chameleon might change into black color if it feels cold. Similarly a chameleon might turn light color to protect from sun’s heat.

Chameleons turn into bold colors to communicate with other chameleons. Males change into dark colors to express their anger. Whereas females change colors to let the males know that they are willing to mate. Owners of chameleons know the mood of their pets just by observing the changes in colors.

HOW DO THEY CHANGE COLORS

The outermost layer of their skin is so transparent. Under this skin there are certain cells called as Chromatophores. These chromatophores are filled with different pigments. The deepest layers contain cells called as melanophores , these are responsible for different color shades. The top layer iridophores are responsible for blue and light colors. On top of Idirophores there are two more cells known as xanthophores and erynthophores. These are responsible for yellow and red colors.

These pigments are filled in tiny sacs inside the cells and therefore they are responsible for all the color changes based on their mood. When the color changes the chromatophores are expanded.

![]()

When the seasons change , we will fall ill automatically.

Have you ever wondered why do i fall ill when climate change occurs?

Why do this happen ?

Lets us get into the brief explanation on how climate change and health are related.

According to medical research, adults suffer cold 2-4 times whereas children suffer 5-7 times in a year.

Every three months we see a climate change. So due to the change of the climate the allergens in the surroundings also increase which brings nearly up to hundreds of viruses in the air.

These viruses are mostly responsible for the rise in the temperature in our body. They are also responsible for getting cold.

Common Symptoms of Cold

1) Stuffy Nose

2) Sore Throat

3) Sneezing

4) Watery Eyes

5) Muscle Aches (body pains)

The change in temperatures allows the viruses to develop in the air and perhaps become contagious diseases.

* The most common virus is the Human Rhino Virus (HRV). This virus is responsible for developing colds to 40%.These mainly occur in Spring and Winter.

* Summer season gives people a runny nose and itchy eyes when they are near grass. The immune system gets busy reacting to these allergens causing viral diseases.

* Influenza virus is a flu that develops when the air is dry in winter.

![]()